Create a Personal Budget

There are plenty of ways to set up your budget, but one approach to consider is the popular 50-30-20 philosophy of personal budgeting.

According to the 50-30-20 philosophy of budgeting, 50% of your budget should go toward essentials – things like your mortgage, cell phone bill, groceries, gas, and other bills.

Next, 30% of your budget should go toward your wants. Wants can include things like clothing, dining out, and entertainment.

The final 20% of your budget should go toward savings.

Here is a tool that will help you set your budget using the 50-30-20 method.

Save Money

Entering a new year, or really, anytime you set goals, starting an emergency fund is a great goal. If this is your resolution (even if it's not actually New Year's), head to our blog, New Year’s Resolution: Build Your Savings!

Start Investing

Think of investing as paying your future self. Start by setting a goal to set aside a certain amount of money each month (this can be a part of the 20% of your budget that goes toward savings) to invest.

Consider doing research into a beginner investment portfolio, and looking into working with a professional, accredited financial advisor for assistance.

Make a Will

It might seem morbid, but having a will helps ensure that the assets you have today don’t cause friction for your family should something happen to you.

You can hire an attorney, sure, or you can look into various online resources for templates and other resources to keep expenses down.

Review Your Current Insurance

Is it possible you’re paying too much for insurance? Is it possible there is coverage your need but don’t currently have? From health insurance to life insurance, homeowners’ insurance to car insurance, there are plenty of options available.

Additionally, be sure to review your beneficiaries to ensure they are all accurate.

Talk with your insurance agent, financial advisor, and of course, your family to make sure you have the coverage that makes the most sense for you and your family.

Pay Down Debt

There are plenty of methods people use to pay down debt. Two of the more well-known methods are the avalanche method and the snowball method.

Debt Avalanche Method

With the debt avalanche method, you make minimum payments on all of your credit obligations and use remaining funds to put more money toward your bills with the highest interest rates.

This method will save you the most money in interest and reduces the amount of time it takes to get out of debt. However, it can be more mentally challenging as it can be harder to see the impact you’re making on your debts and stay motivated.

Debt Snowball Method

With the debt snowball method, you make minimum payments on all of your credit obligations and use the remaining funds to put more money toward your bills with the lowest balance.

This method allows you to feel the satisfaction of paying off the “low hanging fruit” and motivates you to keep working your way through your debts to get them all paid off. Unfortunately, this method involves paying more in interest and can take longer to become debt free.

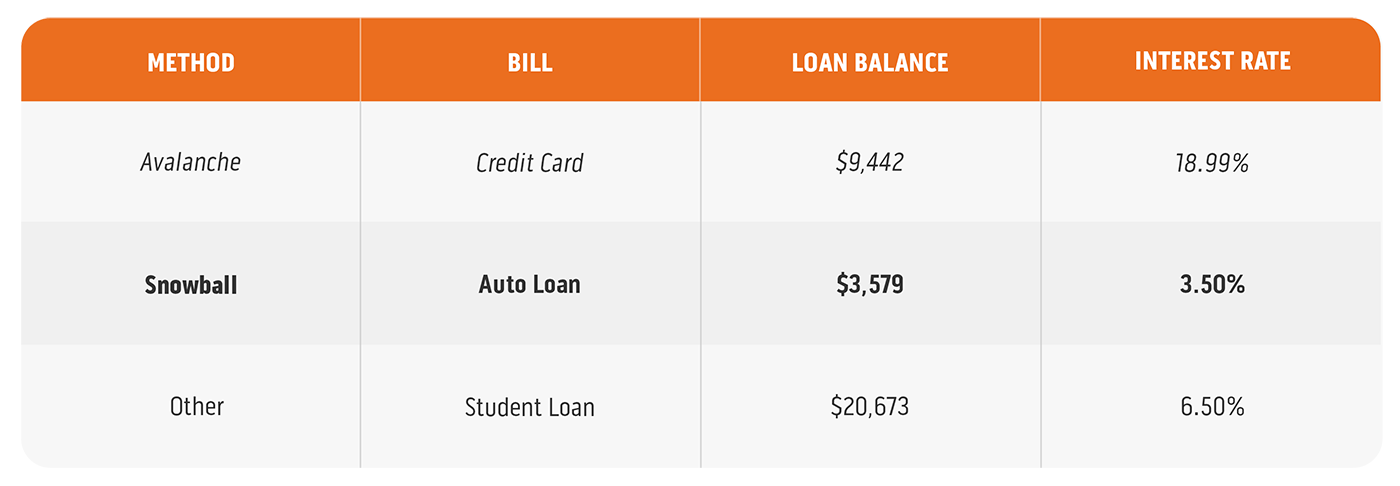

For example, in the chart below, you would focus on paying down the debt that is italicized most aggressively if you were using the avalanche method, and the debt that is in bold if you were using the snowball method.

Maximize Credit Card Rewards

It may seem ironic to talk about using credit cards right after talking about paying off debts – but hear us out.

There is a way to use credit cards wisely – without racking up a bunch of debt in the meantime…if you’re disciplined, that is.

If your credit card has rewards, use that card to pay for as much as you can each month, including your groceries, gas, and even bills.

Then, set up automatic payments to pay off the balance in full each month – if you don’t already carry a balance.

If you currently carry a balance on your credit card, set a reminder to make a payment in the amount of that month’s expenses plus the extra amount you are using to pay it down using one of the debt repayment methods above.

Then, watch your rewards kick in. If you have the option to use your rewards as a payment toward your debt, even better!

Psst...if you're looking for great credit cards, check these out!

Refinance Your Home

Even in a higher rate environment, there’s still a chance you can gain something from refinancing your home.

There are a few different ways you can potentially benefit from refinancing:

- Reduce your rate and enjoy a lower monthly mortgage payment.

- Reduce your rate but continue to pay the same amount as you already are, which puts more money toward principal and helps you pay down your loan faster.

- Reduce your term length, which reduces your rate even further than if you refinance into a loan that would have the same payoff date. You’ll pay even less in interest overall and pay your debt off sooner.

- Get a cash-out refinance – your loan amount may be larger, but the cash out allows you to pay for renovations, vehicle purchases, or other expenses at a potentially lower rate than if you were to get another type of loan for the expenses.

Talk to a mortgage advisor to see if a refinance would benefit you.

Save for College for Your Kids

There are a few ways to save for college. The simplest is to simply set up a savings account on behalf of your child and set aside a certain dollar amount each month toward the account.

This method has the benefit of being simple and safe. On the flip side, there are methods that would help build more interest, meaning more money toward your child’s education, and even have tax benefits.

Some options include a 529 account or an Education Savings Account (or ESA), which can help you save money on taxes, have minimal impact on financial aid requests, and allow you to earn interest.

There are some differences between these two options (and there are other options as well, including IRAs and more), so you’ll want to speak with a financial advisor to help determine the best option for you.